Fixed vs Adjustable Mortgage: A Complete Guide to Choosing

Choosing a mortgage is one of the most significant financial decisions you will make, and the core choice often boils down to two fundamental paths: the stability of a fixed-rate mortgage or the initial flexibility of an adjustable-rate mortgage (ARM). Understanding the fixed vs adjustable mortgage meaning is not about finding a universally “better” option, but about matching the right loan structure to your financial profile, risk tolerance, and life plans. This decision will influence your monthly budget for years, potentially saving or costing you tens of thousands of dollars over the life of the loan. By delving into the mechanics, pros, cons, and strategic use cases for each, you can move forward with confidence, knowing your mortgage is a tool that works for you, not a source of financial stress.

Understanding the Core Definitions

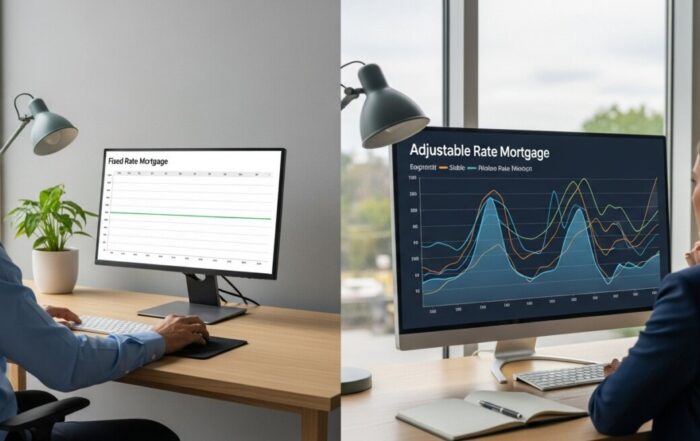

At its heart, the fixed vs adjustable mortgage meaning centers on how the interest rate, and consequently your monthly principal and interest payment, behaves over time. A fixed-rate mortgage has an interest rate that is set at closing and remains unchanged for the entire loan term, whether that is 15, 20, or 30 years. This provides absolute predictability: your payment for principal and interest is a known constant, immune to fluctuations in the broader financial markets. In contrast, an adjustable-rate mortgage has an interest rate that can change periodically after an initial fixed period. This means your monthly payment can go up or down based on movements in a specific financial index, plus a margin set by your lender.

The structure of an ARM is defined by a series of numbers, such as 5/1, 7/1, or 5/6. The first number indicates the initial fixed-rate period in years. The second number indicates how often the rate can adjust after that initial period (usually every 1 year or every 6 months). For example, a 7/1 ARM offers a fixed rate for the first seven years, after which the rate adjusts annually. This hybrid structure is key to its appeal, offering a lower initial rate than a comparable 30-year fixed mortgage for a set time, with the understanding of future uncertainty.

Detailed Breakdown: The Fixed-Rate Mortgage

The fixed-rate mortgage is the bedrock of American home financing, prized for its simplicity and security. Its primary advantage is stability. Once you lock in your rate, you have a permanent, unchanging financial obligation for the core housing cost. This makes long-term budgeting exceptionally straightforward and provides peace of mind, especially in environments where interest rates are historically low or are expected to rise. You are insulated from inflation and Federal Reserve policy shifts that drive market rates upward. This security allows homeowners to plan their finances decades in advance without fear of payment shock.

However, this stability comes at a cost, typically in the form of a higher initial interest rate compared to the introductory rate on an ARM. Lenders charge this premium for assuming the interest rate risk on your behalf. If market rates fall significantly after you secure your loan, you cannot benefit from the lower rates unless you refinance, which involves closing costs and a new qualification process. Therefore, a fixed-rate mortgage is often best suited for buyers who plan to stay in their home for a long time (typically more than 7-10 years), those with a low tolerance for financial risk, and individuals who value predictable payments over potential initial savings.

When a Fixed-Rate Mortgage Is the Strategic Choice

Choosing a fixed-rate mortgage is a strategic move in several common scenarios. First time home buyers who are stretching their budget to afford a home benefit immensely from the payment certainty, as an unexpected increase could be financially devastating. Similarly, individuals on fixed incomes, like retirees, require the predictability that a fixed payment provides. Furthermore, in a low-interest-rate environment, locking in a historically low rate for 30 years can be a tremendous long-term wealth-building strategy. If you are not comfortable with the idea of your housing payment changing, or if the thought of tracking financial indexes causes anxiety, the fixed-rate mortgage is almost certainly your preferred path.

Detailed Breakdown: The Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage is a more dynamic financial instrument designed to offer initial savings with the acceptance of future rate variability. Its most attractive feature is the lower initial interest rate during the introductory period. This can translate to significantly lower monthly payments in the early years of the loan, allowing buyers to qualify for a larger loan amount or free up cash flow for other investments, savings, or expenses. ARMs can be powerful tools for buyers with specific, shorter-term plans.

The mechanics of adjustment are governed by your loan documents. After the initial fixed period, the rate is recalculated based on a specific index (like the Secured Overnight Financing Rate, SOFR) plus a fixed margin. Lenders define adjustment caps that limit how much your rate and payment can change at each adjustment period and over the life of the loan. These caps are a critical safety feature. For instance, a common cap structure is 2/2/5, meaning the first adjustment after the fixed period cannot be more than 2 percentage points up or down, subsequent annual adjustments are capped at 2 points, and the rate can never be more than 5 points higher than the initial rate.

The risks are inherent in the name: adjustability. Your payment can increase, sometimes substantially, after the introductory period ends. This phenomenon, known as payment shock, is the greatest danger of an ARM. Your financial future becomes tied to the movements of economic indices. If rates rise sharply, you could face much higher payments with little recourse besides refinancing (which may also be at a higher rate) or selling the home. Therefore, an ARM requires active financial planning and a clear exit strategy.

Strategic Uses for an Adjustable-Rate Mortgage

An ARM is not inherently risky; it is a tool that must be used with intention. It shines in specific situations. For buyers who are certain they will sell or refinance before the initial fixed period ends (for example, due to a planned job relocation, a military move, or a strategy to buy a “starter home”), the ARM allows them to capture the lower rate without facing adjustment. Real estate investors who plan to renovate and sell a property within a few years often utilize ARMs for this reason. Additionally, individuals with irregular but high expected future income (like medical residents or soon-to-be partners in a firm) may use an ARM to lower payments now, with the plan to refinance or absorb higher payments later when their income rises.

Making the Direct Comparison: Key Factors to Weigh

To move beyond the basic fixed vs adjustable mortgage meaning and make a personal decision, you must evaluate your situation against several critical factors. A side-by-side analysis reveals the trade-offs.

Consider these five key decision points:

- Time Horizon: How long do you plan to own the home? If less than 5-7 years, an ARM’s introductory rate is compelling. If longer, a fixed rate’s stability usually wins.

- Risk Tolerance: Are you financially and emotionally prepared for your mortgage payment to increase? If not, a fixed rate is the only prudent choice.

- Market Conditions: Are interest rates high, low, or rising? In a high-rate environment, an ARM might offer relief with a plan to refinance if rates fall. In a low-rate environment, locking in a fixed rate is attractive.

- Financial Flexibility: Could you afford the payment if your ARM adjusted to its maximum cap? Your budget should be stress-tested against this worst-case scenario.

- Future Plans: Are life changes (family, career, relocation) on the horizon that would alter your housing needs? Flexibility in your loan may align with flexibility in your life plans.

Beyond these points, also consider loan features. With a fixed-rate mortgage, you are essentially done with rate shopping once you close. With an ARM, you must understand its components: the index it uses, the margin, the adjustment frequency, and all the caps (initial, periodic, and lifetime). These details define your risk exposure.

Hybrid and Specialized Mortgage Options

The landscape isn’t purely binary. Lenders offer products that blend features or cater to specific needs. For instance, some loans allow you to convert an ARM to a fixed-rate mortgage during a specified window, for a fee, offering a hedge against rising rates. Interest-only ARMs provide even lower initial payments for a set period (you pay only interest), but they carry higher risk as the principal balance does not decrease. Additionally, government-backed loans like FHA and VA offer both fixed and adjustable-rate options, sometimes with more lenient qualifying criteria. It is crucial to understand that any loan offering a lower initial payment than a standard 30-year fixed mortgage typically does so by deferring cost or risk to the future.

Frequently Asked Questions

What is more popular, fixed or adjustable-rate mortgages?

Fixed-rate mortgages are far more common in the United States, primarily due to the value Americans place on payment stability and predictability, especially for their primary residence. ARMs see increased popularity during periods of very high fixed rates or among more sophisticated, mobile, or investor buyers.

Can you refinance an ARM into a fixed-rate mortgage?

Yes, this is a very common strategy. Homeowners with an ARM often refinance into a fixed-rate loan before their adjustment period begins, especially if interest rates are favorable or they decide they want long-term stability. This requires qualifying for the new loan based on credit, income, and home equity.

What happens to an ARM when the Fed raises interest rates?

Most ARMs are tied to indices that are influenced by, but not directly set by, the Federal Reserve. When the Fed raises its target rate, it generally pushes short-term interest rates higher, which will cause the indices tied to ARMs (like SOFR) to rise. This will lead to higher rate adjustments for ARMs at their next adjustment date, assuming the index has increased.

Is an ARM ever a better long-term choice than a fixed mortgage?

It can be, but it involves significant risk and requires favorable market movements. If you secure an ARM with a low initial rate and market rates fall or remain stable for many years, you could end up paying less over 30 years than with a fixed mortgage. However, this is a speculative outcome that is impossible to guarantee. For most people seeking a long-term home, the fixed-rate mortgage’s guarantee is more valuable than the ARM’s potential savings.

How do I calculate what my ARM payment could become?

You must use the worst-case scenario based on the loan’s lifetime cap. Take your initial rate, add the maximum lifetime interest rate cap (e.g., 5 percentage points), and use a mortgage calculator to determine the new principal and interest payment on your remaining loan balance. Your lender is also required to provide you with a disclosure that shows examples of potential payment increases.

Ultimately, the fixed vs adjustable mortgage meaning is a lesson in financial trade-offs. The fixed-rate mortgage trades potentially higher initial costs for lifelong certainty. The adjustable-rate mortgage trades future uncertainty for immediate savings. Your personal financial map, marked by your timeline, career, risk comfort, and goals, will show you which path leads to a more secure and successful homeownership journey. Consult with a trusted, licensed mortgage advisor who can provide personalized projections and help you scrutinize the fine print, ensuring your final choice is one you can live with comfortably for years to come.

About Daniel Smith

Recent Posts

Fixed vs Adjustable Mortgage: A Complete Guide to Choosing

Understand the fixed vs adjustable mortgage meaning to choose the right loan. This guide helps you secure stable payments or maximize initial savings based on your financial plan.

How Much Down Payment Do You Need for a Mortgage?

Learn how much down payment is needed for a mortgage, from 0% to 20%, and discover the loan types and strategies that make homeownership achievable.

How to Improve Mortgage Eligibility and Secure Loan Approval

Learn actionable strategies to boost your credit, manage debt, and save effectively to improve mortgage eligibility and secure better loan terms.

Finding the Best Mortgage Lenders for First Time Buyers

Discover how to identify lenders with first time buyer programs, low down payments, and exceptional support to simplify your path to homeownership.