What Is a Mortgage Interest Rate? A Complete Explanation

When you apply for a home loan, the mortgage interest rate is arguably the most critical number you will encounter. It is not just a percentage on a page, it is the primary driver of your monthly payment and the total cost of your home over the life of the loan. Understanding what a mortgage interest rate is, how it is determined, and why it fluctuates can save you tens of thousands of dollars and help you secure the best possible loan for your financial future. This comprehensive guide will explain the mechanics of mortgage interest rates in clear terms, empowering you to make informed decisions as you navigate the home buying or refinancing process.

The Core Definition of a Mortgage Interest Rate

A mortgage interest rate is the annual cost you pay to borrow money from a lender, expressed as a percentage of your total loan amount. It is essentially the price of the loan. Unlike fees that are paid once, interest is charged over the entire term of the loan, typically 15 to 30 years. Your interest rate directly determines a significant portion of your monthly mortgage payment, specifically the portion that goes to the lender as profit, separate from repaying the principal loan amount, property taxes, or homeowners insurance.

To illustrate, imagine you take out a $300,000 fixed-rate mortgage with a 6% annual interest rate. In the first month, your interest charge would be calculated as one-twelfth of 6% of the outstanding balance: $300,000 x 0.06 / 12 = $1,500. That $1,500 is pure interest. The rest of your payment that month goes toward reducing the principal. As you pay down the principal over time, the interest portion of each payment gradually decreases, a process known as amortization. This is why, especially in the early years of a mortgage, you build home equity slowly, as most of your payment is servicing the interest cost.

How Mortgage Interest Rates Are Determined

Mortgage rates are not arbitrary. They are set by a complex interplay of macroeconomic forces and individual borrower qualifications. At the broadest level, rates are heavily influenced by the bond market, particularly the yield on the 10-year U.S. Treasury note. Lenders use this as a benchmark. When the economy is strong, Treasury yields tend to rise, pushing mortgage rates up. When the economy weakens or uncertainty rises, investors flock to the safety of bonds, driving yields down and often pulling mortgage rates lower with them. The Federal Reserve’s monetary policy, which targets short-term interest rates, indirectly influences long-term mortgage rates by affecting inflation expectations and economic growth.

On a personal level, your unique financial profile is assessed by lenders to determine the specific rate you are offered. This is where the concept of risk-based pricing comes into play. Lenders evaluate how likely you are to repay the loan. A higher perceived risk results in a higher interest rate to compensate the lender. The primary factors in this assessment include your credit score, loan-to-value ratio, debt-to-income ratio, and the type of property and loan you are seeking. For a deep dive into one of the most significant personal factors, our resource on how credit affects your mortgage interest rate provides essential details.

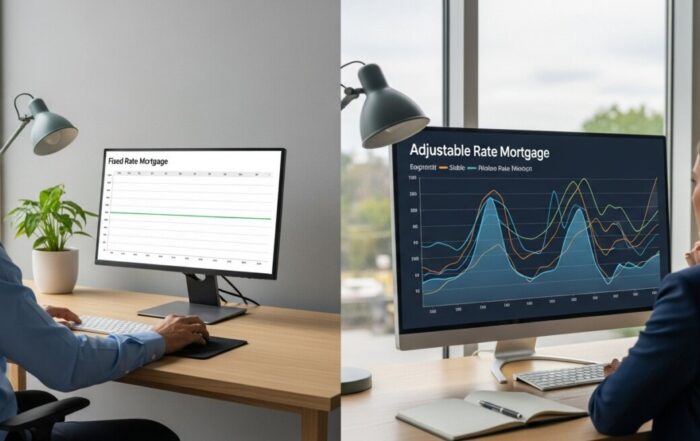

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

The stability of your interest rate over time defines the two main categories of home loans. A fixed-rate mortgage has an interest rate that remains constant for the entire loan term. This provides predictability, as your principal and interest payment never changes, making long-term budgeting straightforward. Fixed-rate mortgages are ideal for buyers who plan to stay in their home for many years or who prioritize payment stability above all else.

An adjustable-rate mortgage (ARM) has an interest rate that can change periodically after an initial fixed period. A common example is a 5/1 ARM, which has a fixed rate for the first five years, then adjusts annually based on a financial index plus a set margin. ARMs typically start with a lower introductory rate than fixed-rate mortgages, which can be advantageous for buyers who plan to sell or refinance before the first adjustment. However, they carry the risk of future payment increases. When considering an ARM, it is crucial to understand the adjustment frequency, interest rate caps (which limit how much the rate can change), and the index it is tied to.

The Real Cost: Understanding Annual Percentage Rate (APR)

While the interest rate is vital, the Annual Percentage Rate (APR) provides a more complete picture of the loan’s annual cost. The APR includes the interest rate plus most of the upfront fees and costs associated with the loan, such as origination charges, discount points, and certain closing costs. These fees are amortized over the life of the loan and expressed as a percentage. As a result, the APR is almost always higher than the base interest rate.

Comparing APRs from different lenders is a more accurate way to shop for a mortgage than comparing interest rates alone, as it accounts for lender fees. However, the APR has limitations. It assumes you will keep the loan for its full term, and it does not include all costs, like appraisal fees, title insurance, or homeowners insurance. Therefore, use the APR as a key comparison tool, but also review the Loan Estimate document line-by-line to understand all charges.

Key Factors That Influence Your Personal Rate

Lenders use a detailed set of criteria to price your loan. Here are the most influential factors under your control:

- Credit Score: This is the most significant personal factor. Higher scores demonstrate a history of responsible credit use and signal lower risk to lenders, resulting in lower rates. The difference between a good and excellent score can mean a substantial rate reduction.

- Down Payment and Loan-to-Value Ratio (LTV): A larger down payment means a lower LTV ratio (loan amount divided by home value). A lower LTV represents less risk for the lender, as you have more immediate equity in the property, which often qualifies you for a better interest rate.

- Debt-to-Income Ratio (DTI): This measures your total monthly debt payments against your gross monthly income. A lower DTI (typically below 43% for most loans) shows you have sufficient income to manage your mortgage payment alongside other debts, making you a more attractive borrower.

- Loan Type and Term: Government-backed loans (like FHA, VA, USDA) may have different rate structures than conventional loans. Furthermore, a 15-year fixed mortgage will always have a lower interest rate than a 30-year fixed mortgage because the lender’s money is at risk for a shorter period.

- Points: You can often choose to pay discount points (prepaid interest) at closing to “buy down” your interest rate. Each point typically costs 1% of the loan amount and lowers your rate by about 0.25%. Whether this makes financial sense depends on how long you plan to own the home.

Strategies to Secure a Favorable Mortgage Rate

Securing a good rate requires preparation and proactive shopping. Start by thoroughly checking and improving your credit score several months before applying. Pay down existing debt to lower your DTI and save for the largest down payment you can manage. When you are ready, get pre-approved by a lender to understand your borrowing power and show sellers you are a serious buyer.

Most importantly, shop around. Get detailed Loan Estimates from at least three different types of lenders: a large bank, a credit union, and an online mortgage lender. Compare the interest rates, APRs, and closing costs side-by-side. Do not focus solely on the rate, ignore the fees. Remember, the quoted rate is often just a starting point for negotiation. If you have a strong application, you may be able to leverage a competing offer to get a better deal. Understanding the associated costs can also help with tax planning, as detailed in our article on the mortgage interest deduction and its tax benefits.

Frequently Asked Questions

Why do mortgage interest rates change daily?

Mortgage rates are tied to the trading of mortgage-backed securities (MBS) in the bond market. This market reacts in real-time to economic data, geopolitical events, and Federal Reserve announcements, causing rates to fluctuate daily, sometimes even hourly.

What is the difference between getting a rate quote and locking a rate?

A rate quote is an estimate of the available rate at that moment. A rate lock is a formal guarantee from the lender that your interest rate will not change for a specified period, usually 30 to 60 days, while your loan is processed. Locking protects you from market increases but may come with a fee.

Should I always choose the loan with the lowest interest rate?

Not necessarily. You must consider the APR (which includes fees), the type of loan (fixed vs. ARM), and your long-term plans. A loan with a slightly higher rate but significantly lower fees might be cheaper if you plan to move or refinance within a few years.

Can I negotiate my mortgage interest rate?

Yes, to an extent. While you cannot negotiate broad market trends, you can often negotiate lender-specific fees and margins, especially if you have a strong financial profile or a competing offer from another lender. It never hurts to ask.

How does refinancing work with interest rates?

Refinancing involves taking out a new mortgage to replace your existing one. You would typically do this when current market rates are significantly lower than your existing rate, allowing you to lower your monthly payment or shorten your loan term. The process involves similar costs to your original mortgage, so you need to calculate the “break-even point” to ensure the savings justify the closing costs. For more on evaluating this decision, explore our guide on key financial factors in mortgage decisions.

Grasping the intricacies of mortgage interest rates transforms you from a passive borrower into an empowered financial decision-maker. By understanding what the rate represents, what influences it, and how it integrates into the total cost of homeownership, you can confidently navigate the lending landscape. This knowledge enables you to ask the right questions, compare offers effectively, and ultimately secure a mortgage that aligns with your financial goals, paving the way for sustainable homeownership and long-term wealth building.

About Daniel Smith

Recent Posts

What Is a Mortgage Interest Rate? A Complete Explanation

Understand what a mortgage interest rate truly is and how it impacts your monthly payment and total loan cost. This complete explanation helps you secure the best possible loan.

Mortgage Pre Approval Explained: Your Home Buying Roadmap

A mortgage pre approval defines your true budget and strengthens your offer with sellers. Learn how mortgage pre approval works to become a competitive buyer.

Fixed vs Adjustable Mortgage: A Complete Guide to Choosing

Understand the fixed vs adjustable mortgage meaning to choose the right loan. This guide helps you secure stable payments or maximize initial savings based on your financial plan.

How Much Down Payment Do You Need for a Mortgage?

Learn how much down payment is needed for a mortgage, from 0% to 20%, and discover the loan types and strategies that make homeownership achievable.